San Diego draws buyers from across the country. Strong demand, desirable weather, and a coastal lifestyle make it one of California’s most competitive housing markets.

That does not mean selling here is simple. Without the full picture, you leave money on the table and time on the clock.

San Diego contains dozens of neighborhoods that perform completely differently from each other.

A home in La Jolla attracts a different buyer than one in City Heights. A condo in Little Italy moves on a different timeline than a single-family home in Santee. A property in Chula Vista faces different buyer expectations than one in Del Mar.

Your specific location shapes your timeline, your buyer pool, and your total costs. Treating San Diego as one uniform market leads to poor decisions and unpleasant surprises.

What Actually Slows Sales Down in San Diego

San Diego has specific factors that extend timelines regardless of how strong the overall market looks.

Older properties in North Park, South Park, and Golden Hill carry age-related problems. Inspectors flag aging electrical systems, original plumbing, roof wear, and foundation concerns in these homes regularly. Every finding gives a buyer a reason to renegotiate, demand repairs, or walk away.

San Diego sits in a high-fire-risk zone. Many properties in the eastern and northern parts of the county fall within designated fire hazard severity zones. Insurance requirements for these properties add cost and complexity for financed buyers. Some insurers have pulled back from California entirely. A buyer who cannot secure insurance cannot close.

Coastal properties face additional scrutiny. Salt air accelerates wear on roofing, siding, windows, and HVAC systems faster than most homeowners realize. Lenders require flood zone determinations and specific insurance on properties near the water. These requirements add steps and time to every coastal closing.

HOA complications affect a large share of San Diego properties. Transfer fees, approval processes, and document requirements vary widely across the city’s many planned communities and condo developments. These steps add weeks to traditional closings.

California’s disclosure requirements are extensive. You disclose natural hazard zones, prior permits, material defects, fire zone designations, and more. Missing a required disclosure creates legal liability after closing.

San Diego’s high property values push many transactions into jumbo loan territory. Lenders scrutinize income, assets, and property condition more carefully at these loan sizes. Any condition issue found during underwriting delays or kills the deal.

The Real Cost of a Traditional Sale in San Diego

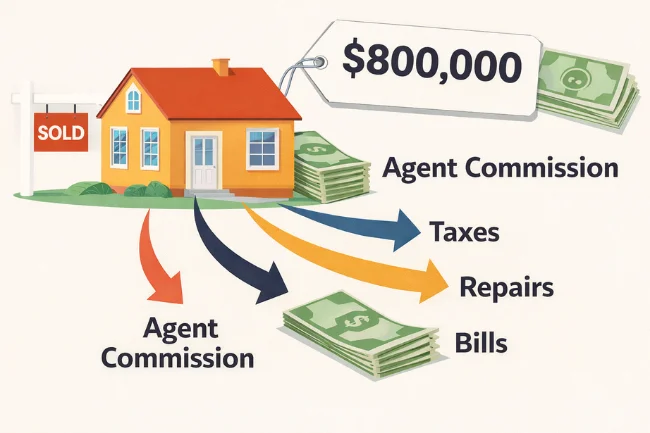

Most sellers focus on their listing price. That number does not tell the full story.

Agent commissions run between five and six percent of your sale price. On a San Diego property, that amount takes a significant portion of your proceeds.

California charges a transfer tax on every sale. San Diego County adds its own charges on top. Both costs come directly out of your proceeds at closing.

California requires a natural hazard disclosure report on every sale. Budget for this cost upfront.

Pre-sale repairs drain your budget quickly on older or coastal properties. A buyer’s inspector finds issues. You negotiate. You spend money on repairs with no guarantee the deal survives.

Holding costs grow every month your property sits. Your mortgage, property taxes, insurance, and utilities keep running whether you have a buyer or not.

Run all of these numbers before you evaluate any offer. Your realistic net from a traditional sale is often far lower than your listing price suggests.

Your Real Options for Selling in San Diego

You have real choices here. Each one delivers something different.

Listing with an agent gives you full market exposure. In active San Diego neighborhoods, a well-priced property in good condition attracts offers quickly. Inspection demands, financing delays, and deal fallthrough risks still apply. Speed is not in your hands.

Pricing aggressively below market draws faster buyer interest. You generate offers more quickly by undercutting comparable listings. Inspection demands and financing delays still apply though. You move faster but lose control of the final number.

Selling to an iBuyer gives you a fast online offer. These companies close quickly in San Diego. Their offers include service fees and shift after their own inspection. The final number often differs from the initial offer.

Selling at auction gives you a fixed date. The outcome is unpredictable. You walk away satisfied or well below your expectations. Auction fees reduce your net regardless.

Selling to a cash buyer removes every variable. No repairs. No agent fees. No financing contingencies. No waiting on a lender. You get an offer, pick your closing date, and close. For homeowners who need to sell a house fast in San Diego, this puts the full timeline in your hands.

How a Cash Sale Works

You contact a cash buyer and share your property details. The buyer reviews your information and presents a cash offer. You take time to review it with no pressure to decide on the spot.

If the offer works for you, you pick your closing date. That date fits your schedule and your plans. On closing day, the transaction completes and you receive your payment.

You fix nothing before closing. You stage nothing. You host no showings. You wait on no lender. The buyer takes your property exactly as it sits today.

San Diego Situations That Point Toward a Cash Sale

Your situation may fit one of these directly.

Your property needs significant repairs and you lack the funds or time to address them before listing. A cash buyer takes the home in its current condition without using findings as leverage against you.

Your property sits in a high-fire-risk zone and insurance complications make a financed sale difficult. A cash buyer does not depend on a buyer securing insurance before closing.

You inherited a San Diego property and live outside California. Managing repairs, coordinating showings, and handling California’s disclosure requirements from another state is a burden most people do not want. A cash buyer handles the process without your constant involvement.

You own a tenant-occupied investment property and want to exit. California tenant protections make selling an occupied property through traditional channels difficult. Cash buyers purchase tenant-occupied properties and handle the tenant transition after closing.

You are behind on mortgage payments and need to close before foreclosure advances. A cash sale moves fast enough to get ahead of that timeline.

You need a firm closing date due to a divorce, relocation, or estate settlement. A cash sale gives you that date without months of uncertainty attached.

Questions to Ask a Cash Buyer Before You Sign

Not every cash buyer in San Diego operates with the same integrity. Ask these questions before you commit.

Does the offer stay firm after signing? Get that answer in writing. A trustworthy buyer answers without hesitation.

Are there fees charged to you as the seller? Reputable buyers cover closing costs and charge no commissions. If a buyer mentions fees, get a full written breakdown before moving forward.

Does the buyer have proof of funds? A serious buyer produces this without delay. Stalling on this question tells you what you need to know.

Does the buyer have verified experience in San Diego? A buyer familiar with California’s disclosure requirements, fire zone complications, coastal property lender requirements, and HOA transfer processes handles your transaction without surprises.

House Buyers of America works across San Diego with no fees, no repair requirements, and closing timelines built around your schedule.

How San Diego Market Conditions Shape Your Decision

San Diego shifts with interest rates, seasonal demand, and California-wide insurance changes. During strong periods, well-priced properties in good condition attract competitive offers fast. During slower periods, listings sit longer and buyers push harder on price and repairs.

California’s insurance market adds a layer of uncertainty that did not exist for sellers a few years ago. Properties in fire-risk zones face a reduced buyer pool as insurers limit coverage across the state. Fewer insurable buyers mean longer timelines for traditionally listed properties in affected areas.

A cash sale removes those variables from your equation. Your offer and your closing date do not depend on insurance availability, interest rate movements, or seasonal patterns. You close on your schedule.

Steps to Take Before You List

Write down your property details. Address, current condition, and any known issues like fire zone designation, coastal wear, HOA complications, liens, or deferred maintenance.

Get a clear picture of your insurance situation if your property sits in a high-fire-risk zone. Understand how that affects your buyer pool before you commit to a traditional listing.

Request a no-obligation cash offer from a reputable buyer serving San Diego. Compare that offer against your realistic net from a traditional sale after commissions, repairs, transfer taxes, and holding costs.

Choose the path that fits your timeline and your property’s specific situation.

Requesting an offer costs nothing. It commits you to nothing. You get a real number and make a clear decision based on your actual circumstances.

WELLNESS NOTESBetter Health

Simple weekly tips

WELLNESS UPDATES

Get Simple Wellness Ideas Every Week

Practical health, dental care, beauty, skin care, nutrition and personal growth tips delivered straight to your inbox.

No spam. Just useful wellness ideas and healthy living guidance.

Irfan Ali is the founder of Wellbeing Junction, where he specializes in synthesizing peer-reviewed research into actionable lifestyle guides. By bridging the gap between scientific data and daily habits, Irfan Ali provides evidence-based strategies for skin health, nutrition, and personal growth. Follow his work for trusted, human-first wellness advice.